Findings of the Federal-Provincial-Territorial (FPT) Working Group on Retail Fees, July 2021

Acknowledgements

The Federal–Provincial–Territorial Working Group on Retail Fees would like to express gratitude for the time and effort of the many stakeholders and companies that provided input in order to inform Working Group deliberations, and who agreed to speak to us on an individual basis.

Executive Summary

This document outlines the key findings of the work of the FPT Working Group on Retail Fees, which was established by Federal-Provincial-Territorial (FPT) Ministers of Agriculture in November 2020. The Working Group was mandated to clarify the impact of retail fees with the objective of proposing potential solutions that benefit the entire food supply chain. It engaged with stakeholders and experts by holding over 60 meetings, commissioned research reports by former industry executives and economists, and researched international approaches to similar issues.

Retail fees are payments made by suppliers to many retailers in exchange for the stocking of products on shelves and associated costs. While some fees are generally accepted, an increasing number of others are seen as contentious (such as retroactive or unilateral fees). This has caused tensions in supply chain relationships, especially between processors and retailers, as retail fees have increased in their form and scale, and they have changed in the manner in which they are imposed. Moreover, the lack of predictability and transparency creates uncertainty which some processors indicate has affected their interest in investing, and which primary producers have argued increases costs on suppliers from fees and associated administrative costs, and for which there is a lack of avenues for recourse. . This dynamic can have other effects on the food supply chain, including adding obstacles to market access for small processors and producers, slowing down innovation, and creating supply and pricing challenges for independent retailers. While the general analysis is clear that there is an issue, it is important to note that the private nature of data on retail fees precludes providing a definitive and precise impact assessment.

Canada is not unique in this regard. Several other countries facing similar situations regarding the imposition of retail fees have developed strategies to address issues which have arisen. The United Kingdom and Australia, for example, worked with their retail and processing sectors to develop approaches that recognized the inherent benefit of retail fees and hard bargaining, but sought to ensure that there were appropriate constraints on how fees were levied.

The findings gathered since November suggest that industry is engaged in seeking a tangible solution. Industry has collaborated with the Working Group in providing their perspectives, analysis and advice. More importantly, there have been exceptional collaborative efforts across the supply chain. The result has been a variety of proposals to address this issue that are supported by processors and retailers. Common across all of these is a general sense that retail fees need to be addressed, and that certain principles and good practices such as predictability, transparency, fair dealing, and access to recourse for dispute resolution need to be at the heart of any approach.

Despite the limitations of the data available, this document provides a new base of information and analysis on this issue. More importantly, the Working Group has noted there is a mobilization of the industry to foster better, smoother and more balanced retailer–supplier relations, with positive effects for the entire food supply chain.

Section 1: Context

Background

Outside of the food sector, retail fees are a little-known facet of how products are brought onto retailers’ shelves. Yet, the issue of retail fees and trade practices between grocery retailers and food suppliers has been debated in the Canadian food industry for decades. In recent years, the topic was raised by stakeholders at various Parliamentary committees. Between November 2020 and February 2021, the Standing Committee on Agriculture and Agri-Food, in a study on the food processing sector, heard witnesses from across the supply chain and recommended that “the Government of Canada support the provinces with the implementation of a grocery code of conduct and participate in collaboration with the provinces to its development in line with their jurisdiction and the Competition Bureau’s guidelines”.Footnote 1 It suggested that retail fees (along with a challenging regulatory environment, tight labour markets, and transportation issues) was one of the main challenges for the sector. The Standing Committee on Industry, Science and Technology echoed this call in June 2021.Footnote 2

In 2017, the Competition Bureau concluded an investigation to evaluate whether certain policies related to retail fee practices enforced by Loblaw Companies Ltd. (Loblaw) against its suppliers raised concerns under the abuse of dominance provisions of the Competition Act. The Bureau noted that hard bargaining by a customer is not anti-competitive under the Competition Act on its own, and may in fact result in benefits, including lower prices for consumers. While a number of Loblaw's suppliers suggested that Loblaw’s policies had caused them to engage in the types of strategies that would impact the degree of competitive rivalry among retailers, the Bureau concluded these allegations were not sufficiently supported by the full body of evidence collected. In 2020, one producers’ association requested that the Competition Bureau open an investigation into potential anti-competitive collaboration by large retailers in response to new retail fees imposed in the summer of 2020. The Competition Bureau closed the investigation as there was insufficient evidence to determine if there had been a breach of the Competition Act.

In 2020, the timing of new retail fees, combined with challenges and costs associated with the COVID-19 pandemic, resulted in increased attention being paid to the impact of retailer practices on the rest of the food supply chain. Stakeholders, including producers, processors, and some retailers, formally called on the federal and provincial governments to take action to ensure fair, transparent and predictable business practices for the agri-food industry.

As a result, FPT Ministers of Agriculture agreed to discuss the concerns of processors, producers and independent grocers regarding increased retailer fees and the need for balance in the supplier-retailer relationship at their annual conference on November 27, 2020. During this meeting, an FPT Working Group on Retail Fees was established by unanimous agreement. Its mandate was to

“…consult with experts and industry members to clarify the impact of the announced fees. The objective is to target potential solutions that benefit the entire food value chain. To support the working group’s discussions, FPT Ministers call(ed) on industry to actively contribute to the development of solutions that will help ensure that Canada has the appropriate conditions for all supply chain partners to prosper. Ministers asked that the working group begin its work as soon as possible in order to propose concrete actions at the next Ministers meeting in July 2021.”Footnote 3

This document is the result of the consultations, research and deliberations of the FPT Working Group on Retail Fees. As part of its mandate, the FPT Retail Fees Working Group, led by Agriculture and Agri-Food Canada and the ministère de l’Agriculture, des Pêcheries et de l’Alimentation (MAPAQ) undertook an ambitious engagement plan from December 2020 to May 2021. They met with over 45 experts and stakeholders, including primary producers, processors, grocers, wholesalers and other groups, and held over 60 meetings. Provincial members of the FPT Working Group also met separately with regional and local stakeholders to solicit regional and provincial perspectives.

The document aims to provide a brief description of the state of retail and food manufacturing in Canada, followed by a qualitative and, where possible, quantitative assessment of both the direct and indirect impacts of retail fees on the supply chain. It raises considerations for possible solutions based on the experience of comparator countries while taking into consideration the unique Canadian context, and it summarizes progress made to date within industry in proposing solutions with regards to the issues laid out. The document concludes with a list of main findings of the Working Group to date so that FPT Ministers may consider next steps.

Section 2: Background on the Sectors

The Canadian Retail Sector

Canada’s grocery retail sector plays a significant role in supplying food to Canadian homes. The supermarket and grocery sector is composed of more than 10,100 stores,Footnote 4 with 451,200 employees,Footnote 5 and revenue of $108.2 billion in 2020.Footnote 6 The top three traditional food retailers (Loblaw, Sobeys, Metro) and top two general merchandise retailers (Walmart and Costco) hold an estimated 80% of the grocery market share of sales in 2020Footnote 7. All three traditional retailers are Canadian based, with Loblaw and Sobeys operating across the country, and Metro operating exclusively in Quebec and Ontario.Footnote 8 In relation to the United States (see Annex B on international experiences) Canada’s grocery sector is concentrated. There is also considerable vertical integration in the food retail sector, with large retailers owning their wholesalers and distribution centres which supply their own stores, as well as independent retailers, including franchises and non-franchises. For example, Loblaw has 532 independent merchants operating franchises under various banners, while over 40% of Sobeys’ 1,500 stores are either franchises or affiliates.Footnote 9

The Canadian food retail sector is also dynamic and competitive, with market shares of large retailers changing over time, and the share of independent and specialty food stores increasing in recent years, from 16% in 2014 to 21% in 2020.Footnote 10 Independent retailers play a significant role in Canada’s food supply, and make up a large part of grocery retailers in Canada. According to the Canadian Federation of Independent Grocers, they have 6,900 members, including some franchises. According to analysis prepared for the Canadian Federation of Independent Grocers (CFIG) in 2015, the independent grocery industry contributes approximately $5.5 billion to gross domestic product, accounting for 2.7% of total retail trade, and employs almost 68,500 workers.Footnote 11

Independent retailers fall under two groups – non-franchised locations (fully independent), and franchised locations. Non-franchised locations purchase directly from manufacturers and self-distribute, while franchises operate under a large retailer’s banner and benefit from terms and conditions negotiated by the franchisor and the manufacturer for most of its supply. In 2015, the survey of CFIG members reported that 41% of survey respondents were single location independent retailers, 22% had two to three store locations, 17% had four or more locations, and 19% were franchisees. In 2018, the share of sales from independents was greatest in Quebec, accounting for 63% of sales. Ontario had the second highest share at 38%, followed by Saskatchewan (30%), Manitoba (28%), and British Columbia (27%). Alberta and the Atlantic regions have lower shares (24% and 21%, respectively).Footnote 12

A key driver of retail profitability includes increasing sales volumes and making purchases more attractive to consumers by keeping prices low. Retailers primarily compete on prices, although other factors have become important, such as e-commerce, technology-enabled experience, delivery options, exclusive brands and loyalty programs offering personalized customer experiences. E-commerce has become one of the most important global retail trends, accelerated by the COVID-19 pandemic.Footnote 13

The Canadian Processing Sector

Canada’s food and beverage processing industry is the largest manufacturing sector, with economic activity totalling $125.5 billion in 2020.Footnote 14 The sector accounts for 1.8% of the country’s gross domestic product.Footnote 15 The Canadian food and beverage processing sector is geographically diverse. Ontario and Quebec accounted for 62% of sales in 2019. Regional variations exist, for example, in the Atlantic Provinces, seafood processing is the main subsector. In other provinces (Quebec, Ontario, the Prairies, and British Columbia), meat processing is the main subsector, followed by dairy processing in Quebec, bakery processing in Ontario, grain and oilseed milling in the Prairies, and other food manufacturing, including snack foods, coffee and tea, in British Columbia, based on available data.Footnote 16

Food and beverage processors employ nearly 290,000 individuals across the country.Footnote 17 In general, the food and beverage processing sector is less consolidated than Canada’s food retail sector; however, some subsectors are heavily consolidated, like beef packing and bakery. According to Nielsen data, for many packaged food and beverage categories the largest 4 to 8 manufacturers hold the majority share of category retail sales, and together with private label products, they often account for around 90% of sales. Nonetheless, there are many small businesses, and approximately 93% of food and beverage processing establishments have fewer than 50 employees, although they accounted for only 15% of the total value of shipments in 2018.Footnote 18

Canadian food processors are increasing their level of exports, with Canadian processed agri-food exports reaching $40.1 billion in 2020 with an average annual growth rate of 6.3% since 2011.Footnote 19 Many factors contribute to this increase, including the depreciation of the Canadian dollar relative to the US dollar. Meanwhile, Consumer Packaged Goods (CPG) imports account for an increasing share of the domestic market.Footnote 20 Total imports of processed agri-food products reached $37 billion in 2020, and had an average annual growth rate of 5.2% over the last decade.Footnote 21

Comparing the Retail and Processing Sectors

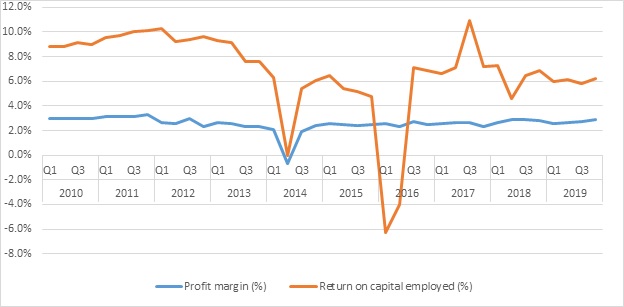

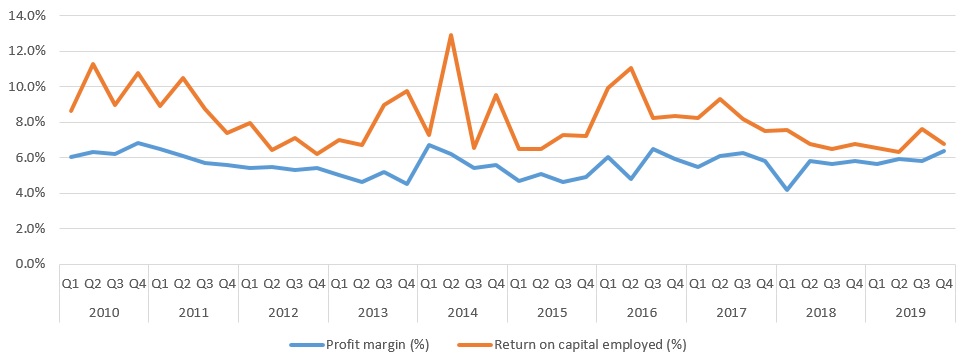

In 2019, Statistics Canada reported operating profit margins of 5.4% for food and beverage processing, compared to 2.8% for food and beverage stores.Footnote 22 Compared to retailers, processors tend to have higher operating profit margins; however, comparisons across sectors are not indicative of the relative health of each sector, given their vastly different business models.

This said, the evolution of profit margins within each sector over time can provide indications of the general health of the sector. As evidenced in the charts below (Figures 1 and 2), profit margins have remained generally stable in both the retail and processing sectors.

Description of above image

| 2010 | 2011 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 3.0% | 3.0% | 2.9% | 3.0% | 3.1% | 3.2% | 3.1% | 3.3% |

| Return on capital employed (%) | 8.8% | 8.8% | 9.2% | 9.0% | 9.6% | 9.7% | 10.1% | 10.1% |

| 2012 | 2013 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 2.6% | 2.6% | 3.0% | 2.3% | 2.6% | 2.5% | 2.3% | 2.3% |

| Return on capital employed (%) | 10.2% | 9.2% | 9.4% | 9.6% | 9.3% | 9.2% | 7.6% | 7.6% |

| 2014 | 2015 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 2.0% | -0.7% | 1.9% | 2.4% | 2.6% | 2.5% | 2.4% | 2.5% |

| Return on capital employed (%) | 6.3% | -0.1% | 5.4% | 6.0% | 6.5% | 5.4% | 5.2% | 4.7% |

| 2016 | 2017 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 2.6% | 2.3% | 2.7% | 2.5% | 2.6% | 2.6% | 2.7% | 2.3% |

| Return on capital employed (%) | -6.3% | -4.0% | 7.1% | 6.9% | 6.6% | 7.1% | 10.9% | 7.2% |

| 2018 | 2019 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 2.6% | 2.9% | 2.9% | 2.8% | 2.6% | 2.7% | 2.7% | 2.9% |

| Return on capital employed (%) | 7.3% | 4.6% | 6.5% | 6.8% | 6.0% | 6.2% | 5.8% | 6.2% |

Description of above image

| 2010 | 2011 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 6.1% | 6.3% | 6.2% | 6.8% | 6.5% | 6.1% | 5.7% | 5.6% |

| Return on capital employed (%) | 8.8% | 7.4% | 8.6% | 11.3% | 9.0% | 10.8% | 8.9% | 10.5% |

| 2012 | 2013 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 5.5% | 5.5% | 5.3% | 5.4% | 5.0% | 4.6% | 5.2% | 4.5% |

| Return on capital employed (%) | 7.9% | 6.4% | 7.1% | 6.2% | 7.0% | 6.7% | 9.0% | 9.8% |

| 2014 | 2015 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 6.7% | 6.2% | 5.5% | 5.6% | 4.7% | 5.1% | 4.7% | 4.9% |

| Return on capital employed (%) | 7.3% | 12.9% | 6.5% | 9.6% | 6.5% | 6.5% | 7.3% | 7.2% |

| 2016 | 2017 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 6.0% | 4.8% | 6.5% | 6.0% | 5.5% | 6.1% | 6.3% | 5.9% |

| Return on capital employed (%) | 9.9% | 11.0% | 8.3% | 8.3% | 8.3% | 9.3% | 8.2% | 7.5% |

| 2018 | 2019 | |||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |

| Profit margin (%) | 4.2% | 5.8% | 5.7% | 5.8% | 5.7% | 5.9% | 5.8% | 6.4% |

| Return on capital employed (%) | 7.6% | 6.8% | 6.5% | 6.8% | 6.5% | 6.3% | 7.6% | 6.8% |

Return on capital is a more accurate measure for comparing two sectors, Figures 1 and 2 shows that there are similarities between these two sectors in this regard, with fluctuations between 8% and 10% growth per year.

Retail Procurement Process

Understanding how most processed items arrive on retail shelves is essential context for understanding the role and dynamics of retail fees in the Canadian food supply chain. Canadian food manufacturer domestic sales are typically made direct to food retailers, or indirectly through food brokers or wholesale distributors. The main line product offering of a manufacturer is marketed directly from a manufacturer to a retailer, particularly in the case of large or medium-sized manufacturers. Distributors or wholesalers, in turn sell to or procure on behalf of smaller retailers. In other words, a large manufacturer may deal directly with a large retailer, but can sell indirectly to smaller retailers through distributors.Footnote 23 Some large retail chains also have their own private label products, which are manufactured under contract with a retailer's own label.

Retail procurement practices are determined by many factors, including the size of the manufacturer, as well as the type of product. Fresh meat and produce, for instance, are typically sold as spot transactions, while packaged and branded foods are more commonly sold under contract, with terms and conditions related to volumes, price, and promotion. For this reason, CPG products are the primary focus when talking about retail fees, and particularly the items found in the centre aisles of grocery stores. CPGs are commonly defined as all packaged and frozen foods as well as soft drinks, and include processed dairy, but exclude processed meat.Footnote 24

Independent research suggested other categories, such as fresh meat and poultry, produce, floral, fresh milk, eggs, prepared foods, and others, have a more limited involvement with trade promotions, although there are concerns in this sector.Footnote 25 Even within the grocery department, different fee amounts are expected from large multinational suppliers in comparison to smaller, regional processors.Footnote 26 All of these practices are ultimately a part of business-to- business relationships, and for this reason they can vary significantly and it is difficult to acquire estimates or generalize the practices across the sectors.

Retail Fees in Canada

Role for Retail Fees in the Grocery Sector

In the context of this document, retail fees are defined as all payments made by a food manufacturer or supplier to a retailer in exchange for stocking the supplier’s products on the retailer’s shelves, and any other related costs. The total dollar spent by suppliers with retailers to get products on shelves is referred to as trade spend.Footnote 27, Footnote 28

The practice of retail fees as a means to allocate increasingly scarce retail shelf space among manufacturers was introduced in the 1980s, an outcome of rapid innovation and growth in consumer goods manufacturing and parallel expansion of retail.Footnote 29 Some literature holds that, from a retailer perspective, retail fees can have cost and risk sharing functions by offsetting some of the risk of taking on new and unproven manufacturer products. These fees may also help streamline the consumer product innovation process by allocating shelf space to manufacturers who are more likely to offer products with a higher probability of retail success.Footnote 30 In the Canadian context, however, it is important to note that retail fee practices have changed over time.

A variety of retail fees now exist to address a range of different activities and practices. A wide number are commonly negotiated by the manufacturer in consultation with the retailer prior to reaching a sales agreement, and typically support sales of the product, while others are not negotiated. For instance, agreed-upon fees may target the marketing of a product, either in flyers or on dedicated shelf space. Types of retailer fees commonly used in Canada are defined in Annex A.

Perspectives on Retail Fees

From the retailers’ perspective, retail fees serve as a risk management tool and as a financial tool. They allow suppliers and retailers to share the risks associated with getting products into the hands of consumers. They also serve as merchandising tactics, providing in-store promotions and optimizing shelf space allocation by offering products that align with consumer preferences. Larger suppliers generally pay higher retail fees overall because they have more products and higher volumes.Footnote 31 However, they pay less to introduce new products because they are more established with brand recognition and less likely to fail. Less well-known manufacturers will pay higher fees to launch new products in order to share the risk in case of failure. However, not all retailers are able to levy retail fees to the same degree, as smaller independent retailers have less bargaining power than large retailers. More typically, they will participate in programs initiated by the manufacturer.Footnote 32 Also, over the course of Working Group’s deliberations, it was alleged that it can be a common practice for large suppliers to attempt to pass on sudden and unpredictable price increases to retailers.

Processors generally understand the need to pay for limited shelf space and most acknowledge there is a portion of trade spend that is mutually-beneficial for suppliers and retailers that contributes toward advertising and marketing of products, increasing sales volume for retailers and processors alike. Mutually-beneficial trade spend (such as, promotions) should serve to increase sales. There are however concerns among suppliers that larger retailers are leveraging their market power to extract fees from suppliers in order to pay for various investments, including infrastructure, which does not benefit suppliers, and does increase profits for retailers at the expense of suppliers. Key examples of fees which have been reported as contentious, or reportedly applied in a contentious manner, includeFootnote 33:

- late delivery fees (varies by retailer, but can cost up to $1,200 per delivery)

- out of stock fees (fines for lost sales can be up to $20,000 per month in high volume categories)

- unloading/lumper fees (third-party unloading services which are typically $500 per pallet)

- unsalable merchandise fee (typically from 1% to 2% of wholesale price) regardless of the reason why the merchandise cannot be sold

- marketing fees, while usually mutually-beneficial, these fees can be administered in a contentious manner (from 3-5.25% of wholesale price)Footnote 34

- early payment discounts (2% discount provided if retailers make an early payment. Occasionally this discount is requested even if the payment exceeds the agreed upon timelines)

- forecasting errors (Processors contend that costs and risks of retailer forecasting errors are passed back to suppliers, though difficult to quantif. If forecasts are set too high, suppliers overproduce leading to inventory write-offs. If too low, suppliers are unable to meet fill rate targets and are subjected to penalties).

It is important to note that not all retailers will charge all of these fees and that the terminology may differ among retailers. However, these practices have led several experts to suggest there are in fact two different categories of fees. While the nomenclature varies, from acceptable and contentious, to cooperative versus non-cooperativeFootnote 35, or even value-creating and value-defeating feesFootnote 36, the intention is to differentiate the impact of the fees. Academics suggest that in order to maintain competitive prices with general merchandizers and online retailers (such as Costco and Amazon), large retailers are exercising their advantageous bargaining power over suppliers by demanding additional costs, which is also argued by suppliers.Footnote 37

The following section focuses on the impacts of more contentious fees and practices, which are the focus of stakeholder concerns.

Section 3: Supply Chain Impacts

The insights and analysis in this section are based largely on the findings of market analysts who were commissioned to explore the economic impacts of retail fees across Canada’s supply chain. It is important to note the availability of pertinent data in this area is limited, as data is often considered sensitive business information and is not publicly available, and it is challenging to draw clear conclusions given the complex dynamics within the food supply chain. There is, however, anecdotal evidence from a variety of supply chain actors, and supported by expert viewpoints, which shows that retail fees contribute to the challenges that occur along the food supply chain. Therefore, quantitative information is provided where possible, and this has been supplemented by qualitative information that was gathered through case studies, input from the independent researchers and extensive engagement with industry stakeholders and experts.

Food and Beverage Processors

As explained in Section 2, some retail fees are considered to be cooperative, mutually-beneficial endeavours that are perceived to add value, and increase sales and profit margins for both manufacturers and retailers (such as advertising fees). However, suppliers and independent researchers maintain that market concentration has facilitated the buying power of large retailers, leading to an evolution of retail fees in terms of not only the type, but also the overall magnitude of these fees. There are claims that fees are imposed in a manner which lacks transparency and predictability, resulting in significant impacts on the industry, particularly on the relationships between retailers and suppliers.

Magnitude of Fees

Due to the confidential nature of retail fee data, information on the level of retail fees is limited. A recent estimate of trade spend by an independent researcher, based on interviews and experience, provides a range of between 15% and 40% of manufacturer’s sales, depending on promotional activities in the category and the supplier’s size, though exceptions occur. In perishable departments, trade spend is estimated to be between 3% and 10% of a manufacturer’s sales, and, as a general rule, the less processed a product is, the closer it is to 3%.Footnote 38

Based on a sample of 19 respondents to the 2018 FCPC Industry Sustainability Survey, a report commissioned by Food, Health and Consumer Products of Canada (formerly Food and Consumer Products of Canada) estimated that, between 2013 and 2017, trade spend increased 22%, more than twice the rate of sales, with an average annual growth rate of 5.1%. In 2017, trade spend in Canada was estimated to be 28% of gross sales.Footnote 39 This was significantly higher than in the US, Canada’s largest trading partner, where retail trade spend as a percentage of gross sales was 18%.Footnote 40

When examining trade spend, food manufacturers appear to face higher trade spend costs than non-food manufacturers. According to the Food, Health, and Consumer Products (FHCP) report, between 2015 and 2017, the share of food processors’ retail trade spend rose from 28.7% of gross sales to 29.7% based on a sample of 22 respondents. In comparison, the share of non-food processors’ retail trade spend rose from 21.1% of gross sales to 23.2%.Footnote 41

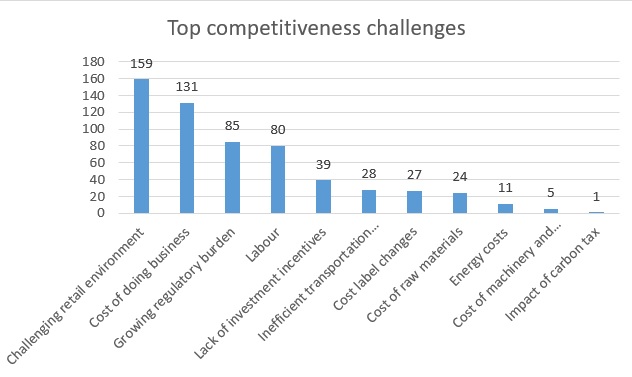

When rising trade spend outpaces sales growth, it can create a less favourable environment for investment. This is supported by the results of a 2019 survey of CEOs, conducted by FHCP, in which a “challenging retail environment” was identified by respondents as the top competitiveness challenge facing the sector among 11 factors (see Figure 3 below). The escalation of trade spend was noted by 95% of CEOs as the leading barrier to investment in Canada.Footnote 42 This said, food processing investment in Canada has remained strong. Based on data from 2010 to 2020, the food manufacturingindustryFootnote 43 as a whole has been investing at a higher rate than total Canadian manufacturing (6.7% compared with 3.1%)Footnote 44, with the bulk occurring since 2018, despite a variety of challenges, including increasing retail fees. Although a 21.1% decline (-$894 million) in capital spending occurred in 2020 in the food processing sector, it was consistent with the manufacturing sector (-22.5%) and it followed considerable increases of $1.2 billion (+64.9%) and $1.1 billion (+35.5%) in 2018 and 2019, respectively.Footnote 45

Description of above image

| Challenging retail environment | 159 |

|---|---|

| Cost of doing business | 131 |

| Growing regulatory burden | 85 |

| Labour | 80 |

| Lack of investment incentives | 39 |

| Inefficient transportation system | 28 |

| Cost label changes | 27 |

| Cost of raw materials | 24 |

| Energy costs | 11 |

| Cost of machinery and equipment | 5 |

| Impact of carbon tax | 1 |

| Note: Score based on ranking where top rank = 5 points and 5th rank = 1 point | |

In a survey conducted by Canadian Manufacturers and Exporters (CME), focused primarily on small or medium-sized enterprises (SMEs) that sell their products through traditional retailers, 64% of survey respondent stated that trade spend costs have risen over the last 3 years, and 50% stated rising costs have negatively impacted bringing new products to market and/or expanding production.Footnote 46

Concerns have been expressed, particularly by SMEs, that within the current retail environment, the high level of these combined retail fees can exclude them from being able to offer their products through major grocery retailers. Instead, they must look to alternative channels (such as independent/niche/discount retailers, and e-commerce platforms) to bring their products to consumers. The impacts on small or medium-sized enterprises are explored further in the Additional issues in supplier-retailer relations section.

“Most of our relationships with small suppliers are done by handshake, and there is no formal contract in place. I am very invested in supporting local farmers/suppliers and I believe in honesty and integrity.” – An independent retailer who engaged with the FPT Working Group.

Manner in which Fees are Imposed

The FPT Working Group heard repeatedly that what is equally concerning for suppliers is the manner in which the more contentious fees are levied, through retroactive, unpredictable and unilateral practices. Suppliers contend these fees are being applied outside of previously negotiated pricing, and hence detract directly from the supplier’s expected margin. These can range from unexpected and unexplained fees, to unforeseen levels of fees, which are simply deducted from the payment for goods.

A survey of Canadian Federation of Independent Business membersFootnote 47 found that charges can also be applied retroactively. Processors noted such practices make understanding these charges even more difficult. Similarly, there are limited avenues for suppliers to question contentious fees and the processes that do exist can be complex and onerous to complete, with limited ability to discuss in person with the retailer. The Working Group has heard that suppliers are also reluctant to contest these fees due to the fear of delisting.Footnote 48 Processors emphasized the importance of accurate and collaborative forecasts to reduce penalty fees and avoid disputes.

While some of the fees are identified as part of the “Core Agreement” between the retailer and manufacturer, the unpredictable nature of other fees and the lack of clarity in how and when they are applied can result in very high costs to suppliers. It was reported that errors in fee assessment are increasingly common, and it is incumbent on the supplier to identify and address these errors.Footnote 49 In addition to the fees themselves, suppliers incur costs to manage and track retail fees. Suppliers have also noted that the purchase of specialized software and hiring of dedicated staff is often required to manage fees from retailers.Footnote 50 The administrative burden of challenging fees, combined with the lack of efficient and objective recourse mechanisms, dissuades suppliers from raising concerns. Industry experts noted this administrative burden may result in productivity decreases.Footnote 51

Additional Issues in Supplier-Retailer Relations

Suppliers have stated that it is very difficult to pass cost increases along to Canadian retailers. While price increases related to higher commodity costs are more likely to be accepted by retailers, suppliers have difficulty obtaining price increases related to other costs such as freight, labour and packagingFootnote 52. Retailers may also request significant justification for price increases including the breakdowns of the input costs. Such requests for information of business value can be perceived by suppliers as a conflict of interest on the part of the retailer, giving them another competitive advantage, as most retailers also own house brands that compete with supplier brands. In addition, there are blackout periods when price increases are not allowed (for example, September to December) and many large retailers require significant advance notice of price increases (for example, 12 weeks minimum) before the increase can be implemented. This means suppliers often have to absorb the additional costs, sometimes for many months.

Suppliers have also alleged in case studies that retailers break pre-existing agreements (such as payment terms) and that, outside of court systems, which processors have stated are too onerous to be useful, there is no recourse when a retailer fails to meet volume targets, promotion strategies or other agreed upon programs.

The competitive landscape is particularly challenging for SME domestic food processors as larger suppliers have more negotiating power with large retailers. Large retailers can exert substantial market power through retail fees over food processors; smaller local processors may find the cost of intensive bargaining difficult to afford. Therefore, retail fees can act as a barrier to acquiring shelf space and local supply can be reduced.Footnote 53 The Working Group has heard small and medium-sized manufacturers express concerns about being competitively disadvantaged by not having the negotiating power to secure the same benefits as larger manufacturers. Large volume incentives, preferred vendor agreements and exclusivity agreements are a particular concern for SME suppliers. By their very nature, larger processing companies are able to pay slotting fees and can more easily access shelf space. For example, large suppliers can provide retailers with significant volume targets, giving retailers an incentive to support their brand over SME suppliers.

It should also be noted retail fees have impacts on supply chain partners across different sectors, such as the supply managed sectors. Under supply management, fees or partial fees cannot be passed from processors to producers since the cost of primary products is administratively set. Thus, food processors under supply management argue they have less flexibility to adjust their business practices when constraints are imposed by retailers. Dairy processors in particular have argued that the impact of contentious retail business practices on dairy processing investment and innovation is compounded given the nature of the supply management system, as well as the nature of their products, which are perishable and have high turnover rates. Additionally, the lack of access to other markets to diversify sales further limits the negotiating leverage of supply managed sectors, in particular with Canadian retailers.

The share of food processors who believe the buying power exerted on them through various requirements and conditions has been an impediment on their ability to compete (for example, restricted access to distribution channels because of listing fees, exclusivity) rose from 11% in 2004 to 24% in 2018.Footnote 54

Investment and Innovation

Retailers regularly see new products, so from their perspective, “innovation is happening and suppliers are in a healthy financial position to develop and launch new products”.Footnote 55 In fact, despite trade spend requirements, 39% of food processing firms with revenues of at least $1 million, reported introducing a new or significantly improved product into the market between 2016 and 2018.Footnote 56

However, according to the companies and associations that the FPT Working Group spoke to, contentious fees create uncertainty and increase risk, making companies reluctant to make new investments, or launch new products in Canada. In fact, according to a 2018 Industry Sustainability Survey — conducted by FHCP — “even when new innovations are brought to market, they are not made in Canada.” Survey respondents reported that in 2017, only 11% of newly introduced items were both developed and manufactured in Canada”Footnote 57. Access to the data and analysis of investments by type would provide further insight.

In addition, independent research confirmed that, “the innovation developed outside Canada is often not brought to Canada. This is due to the high cost of entry and cost of maintaining the brand in this market, many companies cannot justify launching innovation here”.Footnote 58 A negative impact on profits or increased management costs means there are less funds available for investment and to develop innovation. Multinationals stated that they do not always introduce new innovative products into Canada compared to other markets because the payback period for the investment is higher in Canada than in other markets like Europe or the US. This in turn limits the selection of grocery products available to Canadians to some extent, with retail fees being one of many contributing factors.

In addition to the challenges created by contentious fees, domestic food processors, especially SMEs, face increased financial pressures when introducing new products because they have limited financial means to pay the listing fees charged by retailers for new items, which some have noted are higher than for multinationals. For example, one medium-sized processor informed the FPT Working Group that it cost $125,000 per new item for listing fees, and this was on top of the other costs of creating a new product for market (such as equipment, labour and other inputs). Thus, increasing trade spend in areas where processors get little to no return may hinder the capacity of domestic food processors to innovate. And, comparatively, US-based food processors face significantly lower trade spend and have more financial flexibility to market the new products that consumers want.Footnote 59 The lack of transparency in some retail fee practices also limits processors’ reallocation of revenue to innovation.

Evidence shows that uncertainty linked to the manner in which retail fees are imposed, the scale of listing fees in Canada, and forced disclosure of proprietary information, can dampen investment and innovation within Canada’s food processing sector. While the relative weight of trade spending among other factors such as Canada’s regulatory environment is unknown, a key piece of commissioned research contended that “adversarial trade promotion practices are likely a net negative to innovation and investment in Canada”.Footnote 60

Primary Agriculture

Based on an analysis of Statistics Canada data, it is estimated that 20% of Canadian agricultural production goes into the Canadian food retail sector, either as a raw product or as a processed food and beverage product. Of the total raw agricultural products used by the food retail sector, 32% is domestic; and of the total food and beverage manufacturing products used/sold by the food retail industry, 70% is domestically sourced.Footnote 61

Therefore, suppliers include a large number of small and medium-sized producers that sell a range of products — including fruits, vegetables, wine and dairy products — directly to the retail sector. In general, less processed products, perishable goods and primary agricultural products that are sold at a world price, are less affected by retail fees than packaged goods. However, anecdotal evidence from primary producers indicates that listing fees alone for fresh produce may be as high as $6,000 per Stock Keeping Unit (SKU)/brand, a sum that could be restrictive to small and local producers.

The Working Group has heard producers allege that their limited market power prevents them from challenging retailers because of the risk of reprisal. Primary agriculture stakeholders have indicated that some of the particularly problematic issues that arise from this power imbalance include lack of transparency in the application of fees, unpredictable payment terms and lack of contractual terms and obligations that were previously agreed upon. Moreover, producers have suggested that because of their position in the supply chain, they are required to absorb costs associated with fee increases.

What is more difficult to quantify is the impact of retail fees on primary agricultural commodities that are used as inputs to the food processing sector. The role of agricultural products as inputs to processed foods indirectly exposes producers to the effects of retail fee practices by Canadian grocery retailers. In establishing contracts between farmers and processors, prices are negotiated, with prices influenced by many factors including other sales opportunities for farmers and profit margins. Since retail fees will impact processors, either through lower margins, or the need to keep other costs low, it is expected that fees will be passed along to domestic producers to some degree. That said, it is difficult to estimate the impact of fees on Canadian producers, particularly without an in-depth analysis of the Canadian farm share of the food dollar. However, in the US, the farm share was determined to be, on average, 14.3 cents for each dollar spent by consumers on domestically produced food in 2019.Footnote 62 It is important to note that the farm share varies by commodity and is lower when more processing is involved. The impact of retail fees on primary agriculture would therefore vary depending on the type of product.

Independent Grocery Retailers

Independent retailers are key contributors to rural and remote economies in Canada, and to culturally diverse communities in urban areas. They are key suppliers of both food (including local produce) and non-food products to many populations across the country, and they are essential to food security and consumer choice.

Independent retailers do not have the same leverage as large grocers when negotiating with their suppliers, though larger independents may impose some retail fees. In its submission to the FPT Working Group, the Canadian Federation of Independent Grocers called for “fairness and transparency with respect to pricing.” It is alleged that independent grocers are forced to absorb some of the increased costs since suppliers provide larger retailers with hidden discounts and allowances (sometimes at the request of retailers) which are not available to independent retailers. The FPT Retail Fees Working Group was provided with evidence of independent grocers being charged a higher price for supply than their large chain competitors, and some specifically called for a recourse mechanism to address what was referred to as “escalating price discrimination”. In addition, suppliers provide promotional funding to larger retail chains, which they also benefit from due to higher sales volumes. However, CFIG has reported that suppliers will refuse to provide the same promotions to independents in the same market area. This puts independent grocers at a disadvantage in locations where they are competing with larger retailers.

There are concerns among independent grocers about “unfair supply,” and they attribute this to large chains “imposing penalties on suppliers who fail to meet pre-determined, on-time and full deliveries.”Footnote 63 During the height of the pandemic, a large independent grocer confirmed that while supply orders pre-COVID-19 were satisfied at around 95%, in April 2020 service levels dipped to 60%. During the Working Group’s engagement, processors suggested the frequency of ordering may have had an impact on the stock ordered versus stock received by smaller retailers; however independent grocers assert exclusive supply arrangements between suppliers and large retailers were the cause of shortages. Supply challenges from large vendors were also raised, including having to purchase indirectly through wholesalers, or sometimes being refused supply completely, in favour of large chain retailers.

Consumers

Consumer Prices

Processors and retailers have presented different points of view with regards to the impact of retail fees on consumer prices. On the one hand, some large retailers argue that their policy is to keep prices low for consumers, and their suppliers understand the need to share costs in order to meet this goal. In contrast, suppliers claim higher costs in the form of retail fees may lead to a reduction in the number of suppliers entering and remaining in the market, which could in turn lead to a reduction in consumer choice and higher prices for consumers in the long run.

Based on their position in the food supply chain, retailers are, to some extent, food price controllers. They aim to keep consumer prices as low as possible since they compete on price. In fact, stakeholders stated that retailers are reluctant to accept cost increases from suppliers to account for increases in factors including salary, exchange rates and inflation. The Retail Council of Canada explained that grocers push back on price increases to avoid “either further compression of [their] already tight operating margin, or increases to the food prices paid by Canadian consumers”.Footnote 64

Analysis by independent research states food prices can provide information about the competitiveness of the industry. Between 2010 and 2020, average yearly Canadian food retail price inflation was 2%, which is above the 1.65% average per year inflation rate for all items. Additional analysis on the impact of retail concentration on pricing found no evidence that market share is a key driver of either the absolute price of food, or the speed at which food prices increase. Further analysis of regional markets, accounting for other factors that impact prices (that is, quality, demographics, product choice), is necessary to understand the various nuances in how grocery retailers set final prices.

Food Security

The connection between retail fees and food security is primarily driven by concerns about supply, affordabilityFootnote 65 and diversityFootnote 66. This is particularly true in rural and remote communities served by a single or a limited number of independent retailers. Shortages like those experienced during the pandemic and higher prices at independent grocery stores caused in part for reasons described above, can have significant repercussions in rural communities where there are no alternative providers. Many communities rely on vulnerable supply chains consisting of surface and air delivery for food, and limited storage capacity, leading to a fragile “just in time” supply model.

Independent retailers indicated supply shortages are due in part to suppliers prioritizing delivery to larger retailers to avoid fees and/or fines for not meeting established targets. In addition, larger retailers are typically offered lower prices to secure shelf space. This is a key concern among independent retailers who are trying to ensure they can continue providing a variety of food at reasonable prices to consumers, including those in rural and remote communities who have limited options.

Increased retail prices can put additional pressure on consumers, particularly in these communities that already experience higher prices partly as a result of transportation costs and less competition to keep prices down. This is particularly challenging for Canadians in rural and remote regions where incomes tend to be lower and food prices are higher. While the average Canadian household spent 8.0% of their household expenditures on retail food purchases in 2019, the share varied by income quintile, with the share at 11.6% for the lowest income households in Canada. Furthermore, regional differences exist; for example, the lowest income households in Newfoundland and Labrador spent 16.3% of their household expenditures on retail food purchases.

In addition, it has been widely reported that food insecurity affects demographic groups differently, for example, Indigenous populations continue to experience high rates of chronic food insecurity, especially remote and northern fly-in communities. Before the pandemic, an estimated 12.7% of Canadian households experienced food insecurity, with rates particularly high for Black (28.9%), Indigenous off-reserve (28.2%), First Nations on-reserve (48%), and Nunavut (49.4%) households. Households with children headed by women are particularly at risk.Footnote 67

Large Retailers Perspective

Retailers have their own competitive business environment and aim to provide low costs to consumers, however, they have noted that there are challenges related to suppliers providing lower costs to competitors, products arriving below expectations, poor service levels (such as cases ordered versus cases delivered), as well as holding the risk if products do not meet the expected revenue targets. Large traditional retailers are also facing significant pressure to compete against multinational superstores, as well as e-commerce giants. These companies’ investments into e-commerce and increased market share place pressure on traditional grocers to make strategic investments to retain customer loyalty. In recent years, traditional grocery retailers have been losing market share to US-based general merchandizers which are increasing their food offerings, and benefiting from their wide range of products and low prices.Footnote 68

Large suppliers can also benefit from brand recognition and large market share when negotiating with retailers. The FPT Working Group heard from some retailers that large multinational suppliers can exert pressure on them to not levy fees and accept price increases. It was also noted that many times products are delivered without contracts being in place. Several such increases occurred over the course of the COVID-19 pandemic due to a range of impacts on shipping containers, cost of inputs and availability of packaging materials. Large retailers can decide on a case-by-case basis whether to pass these cost increases on to consumers, absorb them through their own operations or negotiate/refuse the increases with suppliers.

Certain fees help retailers manage costs associated with doing business with suppliers, and also serve as an additional revenue streams and a means for reaching sales volume targets which motivate suppliers to continue to do business with retailers. Large retailers claim these fees help ensure suppliers keep commitments on order size and timing.Footnote 69

In terms of innovation, retailers strive to offer new and innovative products to their consumers; however, each new product has an associated risk. From a retailer’s perspective, it can be argued that retail fees reduce the risk that a new product will fail, and listing fees help offset potential losses for the retailer. Successful or anticipated products may benefit from lower fees. In some cases, suppliers provide a market study to demonstrate confidence in their product.

Retailers also informed the FPT Working Group that they do not apply fees uniformly and that they usually consider the size and nature of the supplier. For instance, retailers have flexibility to negotiate with small suppliers, and may be motivated to support local suppliers for a variety of reasons.

Recognizing the benefits that can accrue from sourcing locally, many retailers have implemented local programs where smaller, regional suppliers can access a select group of stores. This can be an entry point for lower volume suppliers. There are no listing fees to be in these programs and they provide an opportunity for small and medium-sized processors to learn how to sell in large retail chains.Footnote 70 However, when it comes to their largest suppliers, many large retailers feel that sharing the costs of retail investments, including infrastructure costs, will greatly benefit their suppliers as well.

Section 4: Path Forward

Solutions in the Canadian Context

Several other countries facing similar situations regarding the imposition of retail fees have taken steps to address the practices of large retailers (these are summarized in Annex B). The Canadian approach needs to consider industry dynamics, geography, production, constitutional divisions of power and the constitutional framework that stems from it. There are numerous examples of industry and government-led approaches to improving business practices, including voluntary codes of conduct (for example, Dispute Resolution Corporation and its code, Voluntary Code of Conduct for Debit and Credit, and Voluntary Scanner Price Accuracy Code). These codes are not directly applicable to the current context, but they can provide inspiration as examples of government and stakeholders collaborating to identify solutions for complex issues.

Founded in 2000, the Fruit and Vegetable Dispute Resolution Corporation (DRC) is a non-profit, membership-based organization that aims to avoid and address commercial disputes in the trade of fresh produce in North America, by providing members with education, mediation and arbitration services. The DRC is an example of an independent, industry-led North American framework, with industry and government representatives on its board of directors.

As retail fees are related to commercial dealings between two businesses, they primarily fall under provincial jurisdiction. Business practices attributed to the scope of retail fees may cross into the competition enforcement regime, an exercise of the federal trade and commerce power, if they meet the legal criteria of reviewable conduct that substantially harms competition. However, previous reviews have not found such evidence. In addition, the federal government has some constitutional power over interprovincial trade in goods, but in this case the primary objective of addressing retail fees would not be to address interprovincial trade.

As such, a regulated or legislated approach would require provincial action. However, stakeholders, the vast majority of which operate nationally, have expressed significant concern about the possibility of disjointed provincial action, which could lead to inconsistent applications and loopholes if some provinces chose not to take action or do so differently. They emphasized the need for a uniform implementation and administration of any option across Canada, particularly if a legislated approach is taken.

Perspectives on Principles

Stakeholders from all segments of the value chain (producers, processors, retailers) have come forward to provide their views and some submitted concrete proposals to the FPT Working Group. Two proposals which have received widespread industry consensus and which have been made public include a joint proposal from Food, Health, and Consumer Products Canada (FHCP) and Empire Company Ltd. (Sobeys), with support from other stakeholders, and a proposal from the newly formed Canadian Food Industry Collaborative Alliance.Footnote 71 Another proposal from the Dairy Processors of Canada and the Conseil des industriels laitiers du Québec includes draft legislation for a mandatory code to be adopted by provincial governments and a model of voluntary code to be supported by the federal government. A summary of these proposals is provided in Annex C. The Working Group also received submission from other stakeholders across the supply chain, including primary producers. All of the industry proposals have called for a mandatory approach, although they diverged significantly in terms of whether this should be done through regulation or not.

While there were differences in the proposed approaches, there was broad alignment on the underlying principles for any action. Stakeholders, for the most part, acknowledge that there are frictions in supplier-retailer relationships. General themes emerged as principles to guide supplier-retailer dynamics, including:

- Commercial relationships should be based on good faith and fair dealing

- The need for transparency and certainty should be recognized in commercial dealings

- Changes to negotiated agreements should be rationalized and communicated transparently in a timely manner, avoiding unilateral or retroactive changes to payments

- Any solution should promote trust and collaboration throughout the grocery supply chain

- A clear and effective dispute resolution mechanism must be available

At a high level, the principles are generally aligned and demonstrate commitment to predictability, transparency, fair dealing and ensuring access to recourse for dispute resolution. Such consensus provides a solid foundation upon which to develop an approach to addressing the issues identified.

Despite broad consensus on principles, many stakeholders proposed a more expansive solution and advocated for the need to rebalance commercial relations and create a level playing field across the supply chain. Primary production stakeholders have raised several issues that they consider to be associated with the significant market power of retailers, such as considerations for the sourcing of products, labelling and private labels products. Independent retailers, among others, have also raised the need for equitable supply and pricing. Some stakeholder groups have also emphasized the principle of reciprocity, whereby if principles are agreed to, they should apply equally to retailers and suppliers of all sizes rather than exclusively to large retailers.

Potential Approaches

Included below are possible approaches to addressing this issue which draw from international examples and which reflect the range of viewpoints in industry. The ultimate goal of most of the proposals and suggestions received was to enhance the resilience of the supply chain for all Canadians.

Voluntary Code of Conduct

- A voluntary code of conduct could include detailed rules to guide commercial relationships and a dispute resolution mechanism.

- Participation: Would be at the discretion of the implicated firms; participants could be bound to conduct themselves according to the Code once committed.

- Development: Could be developed by industry and FPT governments.

- Implementation: Companies or industry associations could incorporate the code of conduct into new or existing Corporate Codes.

- Pros: Voluntary adoption could result in stronger industry commitment because participants volunteer of their own accord. The Code could be more easily reviewed and updated as needed.

- Cons: The outcome of a voluntary code of conduct would depend on the level of adoption and compliance by industry. A low adoption rate may create competitive distortions in the market, if only some stakeholders are subject to compliance costs. Small businesses may be disproportionately impacted by the compliance costs.

Mandatory or Obligatory Code of Conduct

- A mandatory code of conduct would include prescriptive rules to guide commercial relationships.

- Participation: Would be mandatory and mechanisms would be put in place in order to ensure compliance.

- Development: Could be developed by industry and FPT governments, however in a legislated/regulated model finalized drafts would be led by governments.

- Implementation: Two implementation methods were proposed to the FPT WG,

- Legislated: Due to constitutional divisions of power, provinces/territories would need to use legislation or regulation;

- Non-legislated: Industry would implement a code of conduct with mandatory participation (not yet defined at time of writing).

- Pros: Greater likelihood of industry compliance.

- Cons:

- Lack of uniformity in implementation across the country could lead to marketplace distortions;

- There would be an administrative burden for companies in order to ensure compliance with the code, however this may be offset by reducing the administrative burden associated with current practices (such as the time and resources needed to contest and negotiate fees);

- Should either approach include a large variety of supply chain practices and players, concerns have been expressed that the response could be so broad and general as to be ineffective.

Dispute Resolution and Oversight

Either type of code of conduct could be combined with dispute resolution and oversight mechanisms to encourage adoption, resolve conflicts, and in the case of a mandatory approach, ensure compliance. The creation of an independent, confidential and objective form of dispute resolution for all parties to use without fear of retaliation when they believe that they have been mistreated could alleviate friction within the supply chain, while also providing additional services such as education. In other jurisdictions, the roles and responsibilities of dispute resolution mechanisms include a range of functions, including: raising awareness, annual reporting, grading companies on their compliance, mediation/dispute resolution, binding and non-binding arbitration, investigative powers and/or financial penalties.

Section 5: Summary of Main Findings

As per its mandate, through this document the FPT Working Group endeavoured to provide information which clarifies the impacts of retail fees on the food supply chain in Canada. Further research and data analysis, work on potential solutions, and consideration of stakeholder viewpoints will be important in the development of options moving forward. In particular, there remain gaps in order to understand the complexity of this issue, mostly due to the Working Group's lack of access to information of business value. At the time of writing of this document, there was also a lack of quantitative data from objective sources (such as Statistics Canada) as well as a lack of publicly available information from companies in order to paint a clearer picture of retail fee impacts.

Despite these caveats, taking into consideration the vast amount of information the FPT Working Group collected through its engagement strategy, the research reports, and the input and proposals that the FPT Working Group has received from various stakeholders, there is a significantly more solid basis of information today with regards to this issue as a result of this work. In order to inform ongoing discussions and deliberations it is worth noting the following conclusions which can be drawn from the work to date:

- Concentration in the retail sector enables retailers to use their bargaining power to levy a range of fees on suppliers to supply and market their products in store. Recently, retail fees have increased in their form and scale, and they have changed in the manner in which they are imposed.

- The unpredictability and lack of transparency in how some fees are levied, along with limited and often complex recourse for dispute resolution, has led to an overall straining of supply chain relationships from retailers down to primary producers. This has also cultivated the perception of Canada's investment environment as less attractive to some food manufacturing companies.

- There are other secondary impacts of this dynamic, including preventing small processors and producers from accessing the market, impeding innovation, and creating particular supply and price challenges for independent retailers and the local producers they purchase from.

- Facing similar issues, a number of other countries, such as the United Kingdom, have addressed the issue of retail fees via legislated codes of conduct. These processes usually took a number of steps, starting with industry-led voluntary approaches.

- Certain principles and good practices have been recognized by various stakeholders and constitute the basis of a healthy relationship between suppliers and retailers, such as: fair dealing in relationships between suppliers and retailers, predictability, transparency, and access to recourse for dispute resolution.

Annex A: Grocery retailer fees in the food and beverage processing Industry

Below is a non-exhaustive list of various retail fees that may be charged by a retailer to its suppliers. It is important to note that not all retailers will charge all these fees and that the terminology may differ among retailers. Some have simpler supplier-retailer relations, with few (if any) fees, while others implement more complex fee structures and thus have more complicated supplier relationships.

| Fee Name | Description |

|---|---|

| Ad out-of-stock fees | Penalties charged to suppliers should they short product while on promotion. |

| Core/national agreements | In general, Core Agreements between retailers and suppliers establish national sales objectives and provide a bonus to the retailer for attaining the stated objective. These agreements may result in ‘preferential treatment’ since retailers are incentivized to provide more shelf space to suppliers with a Core Agreement, in order to achieve their sales targets. These agreements can make it difficult for new suppliers to compete. |

| E-commerce development fee | A percentage-based fee vendors are required to pay on all products sold by the retailer via its e-commerce platform. The purpose of this fee is to offset investments to accelerate expansion of online grocery distribution and e-commerce capabilities. |

| Exclusivity fees | These typically do not exist on their own but are a negotiating 'chip' which can be swapped for slotting fees. |

| Extended “blackout”/”price freeze” period | Food retailers will unilaterally impose a price freeze ( mandatory 'black out' periods) during which suppliers are forbidden from requesting price increases. These usually coincide with holiday periods (for example, from September to January). If suppliers face a price increase on ingredients during that period, they have to postpone raising their price, and in some instances, they have to provide the retailer twelve weeks’ advance notice. If the retailer accepts the new price, the increase is valid from date of acceptance and is not backdated to the date of initial notification. |

| Extra terms | A 1-2% deduction, applied by some large retailers on its suppliers, to finance store renovations or recent acquisitions. |

| Infrastructure development fee/ strategic acceleration allowance | This fee, typically expressed as a percentage of the cost of goods purchased by the retailer, is charged to vendors to offset the retailers’ infrastructure costs, which could include remodelling of stores and logistics networks, building new distribution centres, and/or implementing new and upgraded systems to improve supply chain efficiencies. |

| Late delivery fees | Fees that are deducted off-invoice by the retailer as a penalty for deliveries being made later than indicated on the purchase order. These fees generally range between $500-$1,000 per order, or $200-$500 if the retailer is given advance notice of the delay. |

| Over and above (O&A) fees |

These fees are a percentage of the suppliers’ sales, typically from 1% to 15% that is deducted by the retailer for marketing support (such as promotional flyers) and distribution. O&A fees are a common practice in the industry but vary from one company to another. They are applied to all suppliers, including established players and newcomers. |

| Payment terms | Generally, suppliers in the industry will offer a 2% reduction on payments made within 10 days, or charge no interest for payments within 30 days. However, some large retailers mandate other standard payment terms (for example, no interest for payments made within 90 days). In addition, some retailers take a 2% deduction from the wholesale invoice, even if payment occurs outside the 10-day window. While this practice is not necessarily a barrier to entry for suppliers, it is a major cost constraint because there is no guarantee of when, or how much payment will be received. |

| Shelf listing fees/slotting fees/listing fees | A ‘shelf listing/slotting fee’ is charged by the retailer to allot shelf space for each food item. These are lump-sum payments due upon approval with no guarantee of minimum sales duration. While it is generally understood that space will be reserved for 12 months, the retailer is not obliged to respect this timeframe. The assessment of Shelf Listing/Slotting Fees is viewed by many suppliers as the most controversial retailer practice because there is no set fee table. These fees are established through negotiations between the retailer and supplier. |

| Unloading (lumper) fees | Drivers are forbidden from participating in the offloading of their trucks in almost all retailer distribution centres. As a result, every centre employs an on-site 3rd party company (known as ‘lumpers’) to handle this service. These fees cost $50 to $500 depending on the number of pallets and time it takes to unload. |

| Unsalable merchandise fees | In the past decade, the liability for product damaged either in-transit or in-store has been transferred from retailer to manufacturer. This fee is charged to the supplier as a percentage of annual sales (for example, 1% to 1.5% for shelf-stable goods) and is usually accounted for in the suppliers’ pricing of most products. |

| Source: List developed with information from various sources, including Simon Dessureault (University of Guelph) and Sean Lippay (Strategic Food Solutions) | |

Annex B: International experiences with codes of conduct for the retailer/supplier relationship

It is important to note that Canada’s main comparator countries have examined and, in many cases, addressed retailer–supplier relationships, which, according to testimony gathered by the FPT Working Group, are increasingly reducing food manufacturers’ perception of Canada as having a positive investment environment. Comparator countries, such as the UK and Australia, have developed retail codes of conduct, serving as inspiration for industry proposed solutions for the Canadian grocery retail sector.

United Kingdom’s Groceries Supply Code of Practice

In 2010, the UK’s national Competition Commission established a mandatory Groceries Supply Code of Practice in response to a 2008 investigation that highlighted the adverse impacts of certain practices by retailers. This Code regulates the practices of large retailers with annual sales of £1 billion, with provisions related to fair dealing, retroactive fines, and clear procedures for de-listing. The Code does not address the level of fees levied and encourages hard bargaining. It also requires retailers to appoint Code Compliance Officers within each retailer to act as a first point of contact for suppliers to resolve disputes. Prior to this current mandatory code, the UK had a voluntary code in 2001 that was developed with industry involvement.

To enforce the Code and ensure further compliance, a Grocery Code Adjudicator was introduced with the power to levy fines on retailers and conduct investigations. However, in discussions with the FPT Working Group, the former UK Grocery Code Adjudicator noted that they relied on creating a culture of compliance, rather than actual enforcement powers. In addition to the company-level Code Compliance Officers who resolve complaints before they ever escalate, the Adjudicator focuses on educating both suppliers and retailers, providing mediation services, and annually reporting and grading retailers’ performance. Only in rare circumstances has the Adjudicator utilized their full powers.

According to annual reporting done by the Grocery Code Adjudicator, this approach has been effective, with 36% of UK suppliers reporting having experienced an issue over the year in 2020, down from 79% in 2014. While resistant at first, large retailers in the UK have also come to support the Code and even advertise their performance to consumers and suppliers.

Australia’s Food and Grocery Code of Conduct

Prior to the current Code, the Australian grocery sector was self-regulated through the voluntary Produce and Grocery Industry Code, which had no prescriptions or enforcement, solely relying on a mediation service. However, in 2014, the federal Australian Competition and Consumer Commission (ACCC) filed proceedings against two large Australian retailers (Coles and Woolworths). Coles was found to have acted “unconscionably” in its attempts to rebate more than $12M AUS from 200 suppliers to recuperate investment costs and subsequent retaliatory actions once some suppliers declined to make paymentsFootnote 72 In response to the public pressure of these cases, the two large retailers worked with Australian suppliers to develop what eventually became the current Food and Grocery Code of Conduct in 2015.

While the Code allows for voluntary adoption (three of the four signatories made up 75% of the market), retailers’ compliance with the Code is mandatory once parties sign on and applies to all suppliers when they deal with signatories. It requires company-level Code Arbiters to investigate, resolve and settle complaints by suppliers. Like the UK Code, it aims to increase the transparency and contractual certainty of retailers’ commercial dealings with suppliers. Like other voluntary and mandatory industry codes in Australia, the Code is overseen by the ACCC due to its authority under the 2010 Competition and Consumer Act. While also under federalism like Canada, these authorities grant the federal ACCC the ability to oversee commercial dealings in sectors using codes of conduct.

According to a 2018 independent review, suppliers reported better relationships with their retailers, despite voluntary adoption. Furthermore, the review also found that large retailers introduced additional initiatives such as conducting their own supplier surveys or providing additional training for their relevant staff. In 2020, the Code was further amended to strengthen the dispute resolution process through a government appointed Independent Reviewer to work with stakeholders to identify and address systemic issues.

Other experiences

In addition to the UK and Australia, other jurisdictions have also addressed these issues in a similar manner. For example, Ireland introduced similar regulations to the UK context under the 2016 Grocery Goods Regulation, which is administered and enforced by its competition body rather than an Adjudicator. Until 2019, the European Union (EU) relied on a voluntary principles-based Supply Chain Initiative to encourage stakeholders across the EU supply chain to adhere to best practices. However, in 2019 the EU shifted to a mandatory approach through a Directive that requires member states to ban unfair trading practices by large food buyers and improve contractual certainty and clarity for suppliers by December 2021.

Annex C: Industry proposals

As an example of the detailed input provided to the FPT Working Group, this annex provides a brief overview of three industry proposals. It is not an exhaustive summary of the views presented by industry.

| Proposal | Food, Health and Consumer Products of Canada (FHCP) and Empire Company Ltd (Sobeys) Grocery Supply Code of Practice for Canada |

Dairy Processors Association of Canada and Conseil des industriels laitiers du Québec Act respecting the relations between grocery retailers and suppliers |

Canadian Food Industry Collaborative Alliance Canadian Food Industry Code of Practice[1] |

|---|---|---|---|

| Proposed approach | Mandatory and legislated code of conduct. | Mandatory and legislated code of conduct. | Mandatory Code, but not embedded in regulation or overly prescriptive. |